The day is finally here. Your teen is getting their drivers license. It’s a major milestone that will affect the family in many ways, some great and some not-so-great. Like when you add your teen driver to your car insurance plan and the monthly premium automatically balloons.

While your rates are guaranteed to increase (teens are considered high-risk drivers), that increase doesn't have to break the bank. Here are 10 ways to get a discount on auto insurance when you add a teen driver to your policy.

10 Ways to Get Discounts on Car Insurance as a Teen

1. Sign Your Teen Up for Drivers Ed

A teen drivers ed course is designed to teach kids safe driving habits. Even if your state doesn’t require drivers ed for a license it’s highly beneficial for novice drivers in terms of lowering their risk of being involved in an accident. And for that reason, insurance companies often give you a discount on insurance rates if your teen has completed a course. Additional driver safety classes can apply, too.

2. Share the Rewards of a Good Report Card

Drivers ed isn’t the only schooling that matters. If your teen is at least a “B” student, you can often get discounts on car insurance. Students who do well at school are usually good pupils that will easily learn the rules of the road and follow them. You can encourage your teen to get a B average by sharing the savings. They’ll need extra cash for gas money!

3. Get a Better Rate With Multi-Vehicle Family Plans

Will your teen have their own car? If so, you may be wondering if they should purchase a separate policy. In most cases, the answer is no. Many of the factors that allow you to get better rates on your insurance (think: being married or having a good credit score) aren't applicable to your teen. Besides, if your teen did buy their own insurance, you'd still have to co-sign, since it's not legal in most states for minors to enter such contracts.

But here's the good part: If you're adding a new car to your policy, you're likely eligible for multi-vehicle discounts.

4. Buy Used Vehicles With High Safety Ratings

Older, simpler cars with high safety ratings get you better insurance rates. Why? Older cars are cheaper to repair if you have a collision, and safety features, of course, decrease your teen's likelihood of being in an accident and/or getting seriously injured.

If you plan to buy your teen a vehicle of their own talk to an insurance agent before you start car shopping. They can tell you which models will be the cheapest to insure. You can also check out this handy calculator from Insure.com to get a better understanding of insurance premiums by car make and model.

Note: While older cars are typically less expensive to repair, some insurance companies offer discounts for newer cars. Just one more reason why it’s a good idea to talk to your agent about the savings available to you.

5. Compare Auto Insurance From 3 Providers

While you're out shopping for cars, you may want to consider shopping for insurance, too. Even if you like your insurance company, getting a better rate could make a difference. NerdWallet has compiled a comprehensive list of what discounts major insurers offer for teen drivers, so you can compare the options.

The rule of thumb is to compare the plans and rates of at least three providers. But remember that it's usually more cost-effective to bundle policies. If you're not currently paying for all your insurance needs under one carrier, you might consider making the switch to consolidate and save!

6. Compare Primary and Secondary Driver Costs

Once you add a teen to your policy, they'll be assigned as a primary or secondary driver to the vehicles you own. Let's say that you have three people in your family who can drive: you, your spouse and your teen. All three must be listed on your policy. In this scenario, if you have three or more cars, an insurance agent will automatically assign your teen as the primary driver of one vehicle.

To save money, ask your agent if you can make your teen the primary driver of the car that is least expensive to insure. If you only have two cars, the agency will consider your teen a secondary driver to one or both cars, which is usually cheaper than having another primary driver on your policy.

Note: You can't be a primary driver for two cars unless you have more cars than people.

7. Enforce the Importance of a Clean Driving Record

Good drivers are rewarded by insurance companies. That means if your teen starts driving as soon as they're legal and keeps a clean record, you could see those rates continuously drop over the coming years.

That's why's its essential for your teen to do things like take drivers ed, get a learner's permit and practice for hours with you or an instructor. The more knowledge and skills they have, the better driver they'll be!

8. Sign Your Family Up for a Defensive Driving Course

Your teen isn’t the only family member who can take drivers ed. You might be eligible for discounted car insurance rates if you take a driver training course, like defensive driving. For $40 or less you can refresh your knowledge, learn some important defensive driving maneuvers that could prevent an accident and save money on monthly premiums.

9. Green Means Go

If you're in the market for a new car, you can cut spending on insurance (not to mention gas) by going green. Some insurance companies offer discounts for those who own fuel-efficient cars. While you're saving the environment, you're also saving money.

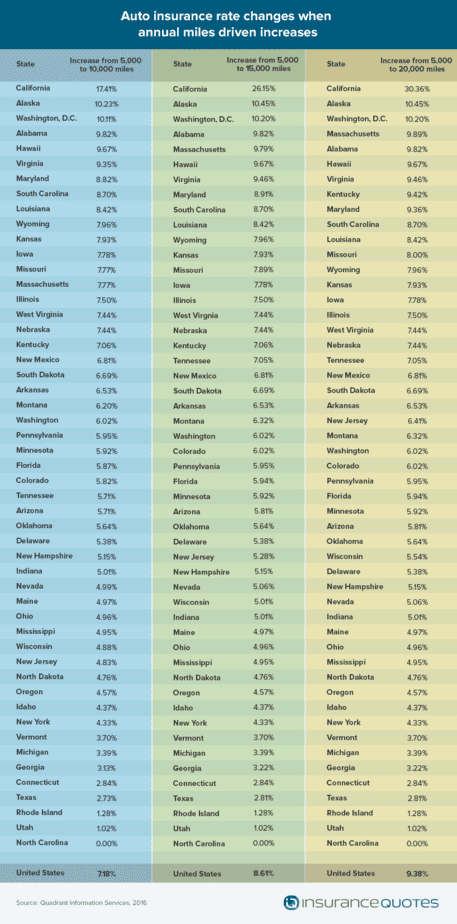

Additionally, you can get low-mileage discounts if you drive under a certain number of miles per year. Check out this awesome chart to see how much you can save on car insurance for driving less in every state.

{kind=link}

Want to take it a step further? Talk to your insurance company about a usage-based program. With a pay-as-you-go model users must install a tracking device in their car. The device monitors mileage, braking habits and speeding tendencies. This same technology is used by many parents to track their teen’s driving and help them practice better driving behavior. Research shows usage-based insurance can save customers up to 10% for simply installing the device and up to 50% while using it.

10. Think Carefully About Raising Your Deductible

Do you have money saved away for an emergency? If so, you might want to consider raising your deductible (the money you have to pay in the event of an accident before insurance kicks in). Doing so would lower your monthly bills, but is not advised unless you have an emergency fund set up. If you can afford to cover your teen if they do get in a wreck, then raise the bar.

Car insurance doesn't have to be expensive with a teenager behind the wheel. There could be many more discounts available to you and your family when it comes to car insurance. Every insurer has different policies and prices, and state laws can affect those as well, so be sure to discuss options with your agent.

*This article was updated on 9/15/2020